I am slightly embarrassed as I recall Paul Simons’ 1975 release of “50 Ways to Leave your Lover”. As a budding 11-year-old, I giggled at the new term “lover”. However, on reflecting back now, having advised hundreds of entrepreneurs and CEO’s, the context rings true – it’s often easier to get into something than it is to get out, and you may need plenty of options to consider.

Whether it’s a relationship or a business there are many choices of exit. And while you might imagine relationships have many more personal complexities the personal and business complexities combined are not to be underestimated when you look to exit your company. In fact, for many business owners, they are “married to the business” or it has become their “lover”. More wholesomely, many hold lifelong relationships at their firm that might be forever changed depending on the chosen route to leave the company. Or if exit is fumbled, their own lifestyle and dreams for retirement may be greatly affected.

Planning for, deciding how, when, where and for how much, you leave your company can be a daunting task. I suspect that’s why so many middle market entrepreneurs and CEOs push off this important step, at times to their peril. (Are you listening boomers – the time is now). We get called on at times to sell companies of surviving spouses or heirs, and on the whole, those exits, or transitions are not nearly as replete in generational wealth creation when the founder or leader has not planned succession well.

Far too often we see CEOs and entrepreneurs focused more on the how much vs. the how and when. I would argue in many respects the market dictates the how much, and none of us knows exactly when our “time” will come, so the how of it is about the only thing we can control 100%.

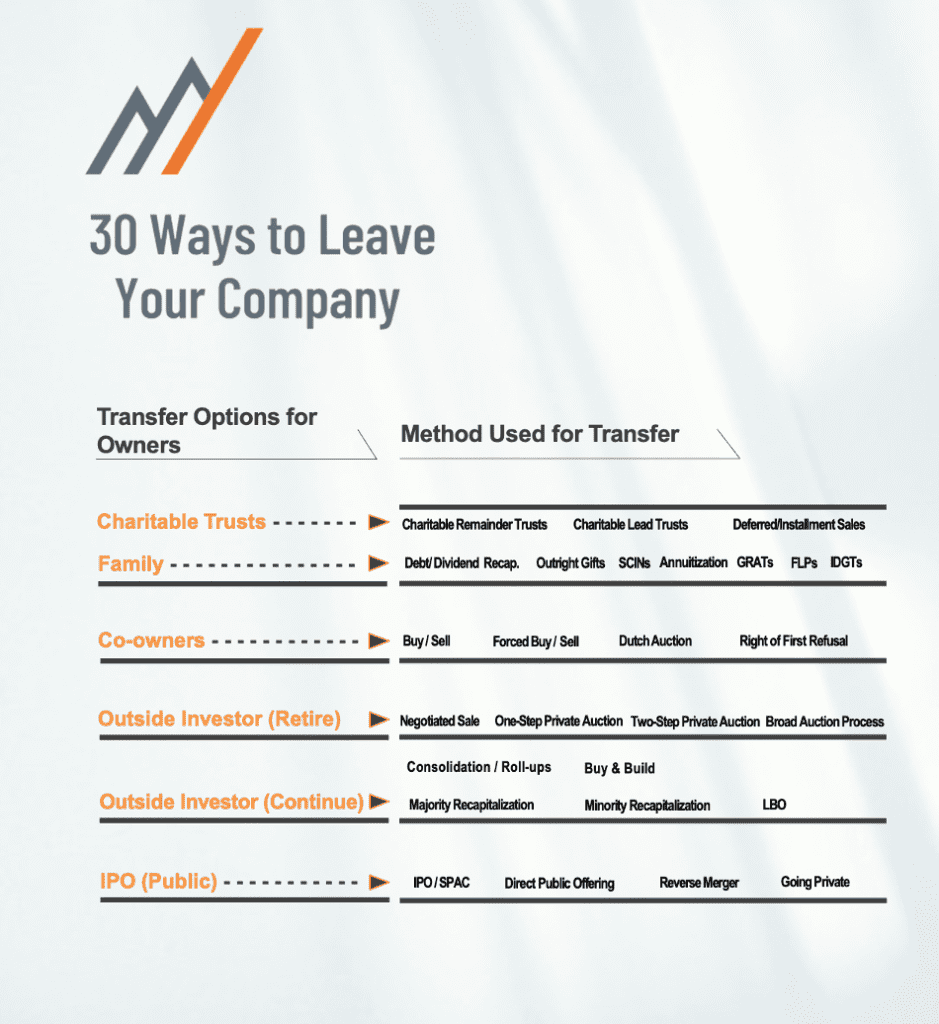

The following is a quick primer on ways to consider leaving your company (transfer options) and ways to achieve your goals (methods used for Transfer). While this list is nowhere replete, we encourage you to have a conversation with your Investment Banker, CPA, attorney and wealth advisor on the appropriate ways and methods you should be thinking about during the process and equally important, what ways may not be available to you. Many of these methods may not be available once you are “in the deal” so if you value minimizing your potential tax liability the time to plan is now.

Reach out to discuss the best path for your company to grow or build generational wealth through the recapitalization or sale of your private company. 253-370-8893 | Craig.Dickens@meritinvestmentbank.com | @MandAexit

Craig Dickens, CEO Merit Investment Bank

Craig is responsible for setting the firm’s vision, creating a culture of boutique personalized service, and recruiting experienced investment bankers to build the Merit Investment Bank team nationally and internationally. Mr. Dickens has advised many leading companies and participates on several middle-market company boards.

Having participated in every kind of business dynamic from start-up to IPO, merger to dozens of acquisitions in his own entrepreneurial career, Mr. Dickens serves clients by guiding them to strategic growth, business optimization, and profitable exit.

Merit Investment Bank is a leading boutique investment bank focused on entrepreneurial middle-market companies. Merit Investment Bank executes sell-side M&A, buy-side M&A, capital advisory services, debt and equity capital raises, corporate finance, and valuation services. www.meritinvestmentbank.com

0 Comments